As we entered 2026, rumblings of significant supply issues affecting memory and storage began to grow. As we move into March, we are seeing real-world impacts, including large price rises, long lead times, and unprecedented changes to commercial agreements. There is a lot to unpack on this topic, so please take some time to understand why this is happening, its impact, the misconceptions, and the mitigation strategies.

The TL:DR is as follows:

• AI Demand for High Bandwidth Memory (HBM), driven by large orders from OpenAI and other Neo Cloud Providers, has consumed around 70% of the world's fabrication capacity.

• This has caused a global capacity crunch on DRAM (server, laptop and networking memory) and NAND (laptop and enterprise storage).

• Logistics friction has significantly driven up the price and reduced the availability of all IT equipment. This has led to budget challenges and long delivery lead times.

• The shortages are expected to last at least 18 months (into mid-2027).

• The Impact is a significant organisational risk and demands a detailed response plan.

So, what is happening?

To understand why this supply crunch is different from previous challenges (such as COVID, the last example), we need to go back to around October 2025. It is important that we understand why this time is different, as it affects the response plan.

When it comes to memory and storage fabrication, there are only three principal players: Micron, Samsung, and SK Hynix. Their fabrication plants can normally produce both DRAM and NAND Flash and are cleverly designed to allow dynamic changes in the quantities of each. This design has enabled the fluid production of both components for years and has provided flexibility to meet changing demands.

AI workloads have driven an increased demand for High Bandwidth memory (HBM). The challenge is that HBM takes materially longer to produce than standard DRAM or NAND, by an estimated 3x. Its creation also has higher failure rates, with a knock-on effect on production capacity. Another influencing factor worth noting is that HBM has a much higher profit margin for manufacturers, which helps determine where those limited fabrication plants would direct production. While the fabrication plants are flexible in switching the types of components they produce, overall capacity still has a fixed upper limit.

Now that we understand the mechanics behind the scenes, we can follow the timeline below to see the impact we have today.

So, in summary, OpenAI placed an order for HBM, consuming 40% of global capacity through to 2029. NEO and hyperscale cloud providers follow suit as we approach the end of 2025, and we estimate that capacity consumption will reach around 70%. These orders force those fabrication companies to pivot production capacity to HBM, as it’s more profitable, and they have large forward-looking orders to fulfil.

This is now the crux of why all other types of DRAM and NAND are in significant constraint. Fabrication capacity is tied up producing that high profit, HBM, leaving reduced capacity for other types of memory and storage production.

It is also the critical reason this challenge is different from previous ones: the fundamental issue is physical capacity in the factories! While new fabrication plants are being built, they will take 18-24 months to come online.

Common Misconceptions

One thing we have been seeing is widespread misinformation in the market that could lead decision-makers to take the wrong turn and suffer significant consequences down the road. Here are the three main ones that seem to keep cropping up.

COMMON MISCONCEPTION #1

This is a memory shortage; only servers in my data centre are affected.

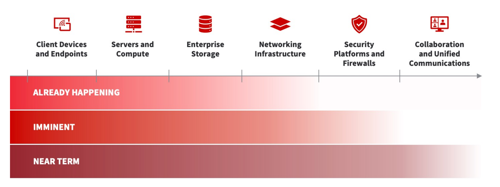

While Server memory is the obvious impact, hopefully, understanding the source of the issue (see above) shows that anything with Memory or NAND storage will be impacted. This means that most IT equipment will be impacted, Client Devices, Servers and Storage are being impacted today. As we move deeper into 2026, this will expand to cover switching (packet forwarding requires memory), firewalls (think of those packet inspection engines), and, finally, collaboration and Unified Communications.

We can see how the impact will escalate across the full domain of IT services throughout 2026 in the image below.

COMMON MISCONCEPTION #2

We’ve navigated constraints before. I can wait this one out.

The problem is that during COVID, the supply issue at those three factories was caused by workers not being able to enter the facilities. This meant the solution was waiting for working practices to return to normal. This time, we are facing a fundamental capacity issue, and the solution is to build more fabrication plants, a process that will take at least 18 months, and then that new supply must make it into the world. This makes this time very different to the post-COVID challenges and needs to be top of mind for every organisation that has any infrastructure requirements in 2026 or 2027

COMMON MISCONCEPTION #3

Moving everything to the cloud will protect me from the shortages.

In the short term, a lift-and-shift to the public cloud could unlock additional capacity in on-premises facilities. Solutions like VMware in the Public Cloud (AVS in Azure, for example) or Nutanix (NC2) can provide access to hardware capacity to augment on-premises demand. The long-term commercial impact will likely be considerable, so it should attract careful planning.

Cloud providers will face the same global component shortages and cost pressures as server and storage manufacturers. As the costs of critical components (particularly GPUs, DRAM, SSDs, and high-capacity HDDs) continue to rise, cloud infrastructure costs are expected to increase as well. We have already seen an impact on AWS pricing and Azure availability.

Watching out for this potential future price shock will be critical.

The impact Today and Next Year

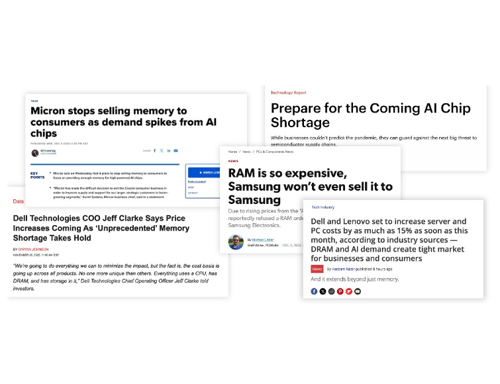

The news has been filled with the impact, from the end of consumer memory lines like Crucial to dramatic changes in ordering and commercial agreements. Three key impacts should be top of mind for anyone planning projects for the next 18-24 months.

30%+ Price Rises: Simple economics: supply and demand are driving prices higher, and we are seeing this change week by week.

6+ Month lead times: For equipment with constrained components, lead times can be upwards of 6 months.

Commercial Agreement Changes: For the first time I can remember (to many years!), we have new commercial terms from many OEM providers. These terms allow for price changes between the time an order is accepted and the time it ships!

The Organisational Risk!

What does all this mean in real terms for both IT and non-IT decision makers? Simply put, it’s Risk at an organisational level based on four core factors.

Commercial Impact: Equipment will cost significantly more during this period; on average, we are seeing increases of 20-50%. This will impact budgets, affordability, and/or bottom-line profitability. All factors that need to be addressed head-on.

Delayed Strategic Projects: Increased prices or equipment shortages can delay strategic projects. Expanding capacity to meet consumer demand, opening new office locations or launching new services to maintain market advantage will become challenging.

Forced Architecture Changes: Architectural standards enable smooth operations, consistent SLAs, and cost control. As pressure on equipment rises, we could end up with forced changes to these standards. Hard choices between maintaining standards and accepting whichever manufacturer has stock will lead to future strategic technical debt, increased operational overhead, and possible platform performance issues.

Security & Compliance Impact: Even if the impact is not new projects, many rolling upgrade cycles are aligned with End of Life or End of Support timelines; missing these refresh cycles could easily lead to security or compliance gaps. Given the state of cyber threats, an overall weakened security posture is not a pleasant thought, but it could pose a risk to your organisation's survival. We also need to consider any regulatory or supplier compliance challenges that validated platforms may face if material changes are made to underlying components.

The risk to every organisation should not be underestimated; without a detailed mitigation plan, it could lead to serious challenges. We believe every IT decision-maker needs a detailed strategic plan to mitigate the impact through to the end of 2027. Missing delivery of that new strategic project could be the difference between being a market leader and a laggard.

Mitigation strategies

How do we tackle these challenges?

There is no single silver bullet that will mitigate the risk, but the following five areas should be top of mind for all decision-makers. The core component is to build a strategic plan as soon as possible.

Strategic Planning & CARA

Without a clear, documented view of all projects in flight or planned for the next two years, it will be impossible to understand their potential impact. Our teams have been delivering strategic planning workshops covering two high-level horizons.

Phase 1: Planning for Efficient Growth

a. Prioritise Projects

b. Assess Current Capacity and Optimisation

c. Prioritise Business Critical Workloads

Phase 2: Be Proactive, Remain Flexible

a. Identify & Repurpose Over-Provisioned Environments

b. Forecast & Secure Inventory

c. Lock In Pricing

d. Review Alternative Options & Configurations

e. Review Commercial Frameworks

Planning for efficient growth covers the foundation components of mapping projects to current capacity and architectural principles to ensure we have a clear foundation of information to build from. One core component of this approach is our Capacity Analysis and Reporting Assessment (CARA), which provides you with the data and technical expertise to extract the best from your current infrastructure.

The second phase then focuses on the five key elements listed above, aligning actional outcomes to each project or risk identified during phase one. Phase two usually requires regular review to align to the rapidly changing landscape. Our position as independent (not single-vendor-aligned) advisors and our scale across all major vendors enable us to deliver insights and mitigation strategies unavailable to others.

Commercial Moves

One core element of mitigation will be commercial in nature and focus on securing pricing and inventory ahead of any critical project demands. Leveraging the capabilities of our Logistics and Technology Centre (LTC) can enable Stock Holding of critical inventory, helping mitigate volatile supply. This stock can then be delivered by our managed just-in-time logistics to most global locations, with or without pre-configurations to meet ongoing project needs.

Couple this with a wide range of payment solutions and our scale leverage with vendors, and we can build a model that allows you to secure stock while mitigating the commercial shock to the organisation.

Technical quick wins

The second area of mitigation will be to review technical quick wins, falling into three core buckets.

DRAM: For years, we have benefited from the versatility of virtualisation technologies. This, unfortunately for many, has led to a proliferation of virtual machines, many of which are significantly over-provisioned. For a long time, DRAM has been 'cheap', and it is easy to throw resources at performance to capacity challenges. This presents an opportunity to run optimisation assessments and explore areas for memory reclamation, resizing new platforms, or leveraging new memory-sharing technologies.

Storage: We have all put off those difficult conversations about what data we should keep or delete. Now could be a good time to engage your line-of-business units and define a new data lifecycle approach.

Maintenance Services: If equipment is approaching the end of its support and a new supply cannot be secured in a timely or cost-effective manner, consideration should be given to third-party maintenance services. Such services can mitigate the risk of security gaps or equipment failures while a new supply is sourced.

ServiceWorks Cloud

More strategic technical wins could come from examining partner-provided private cloud platforms, such as our own ServiceWorks Cloud. While we are not immune to the supply challenges, we do have spare capacity today and mitigation plans in place for future demand. ServiceWorks Cloud is a UK sovereign cloud solution offering IaaS and PaaS services to support both traditional virtual Machine workloads and modern Kubernetes applications. With over a decade of proven delivery and strong connectivity to the major hyperscale providers, ServiceWorks Cloud could offer a future for appropriate workloads.

Architecture choices

We need to design for component substitution by default. The best approach is to treat memory and storage as constrained resources for the foreseeable future (this might not be the last time we see constraints) and to avoid single-SKU or single-vendor dependencies. Look at your architectural principles and define upfront where you can introduce choice and flexibility without compromising compliance, security or operations.

Workload placement strategy is another area for consideration, pushing bursty/elastic workloads to environments where the supply chain doesn’t gate you (often cloud), while protecting predictable baseload on-prem. There has never been a more relevant time to review Hybrid strategies and consider technologies such as AVS, VMC on AWS, or Nutanix NC2.

Conclusion

AI demand for high-bandwidth memory has driven up costs for critical IT equipment; at the same time, lead times are volatile, posing a risk to key initiatives. This is especially prevalent in projects that are underpinned by end-user compute, servers, storage, networking, and security devices.

Building a strategic plan to mitigate these challenges should be top of mind for every organisation. Unlike previous supply challenges, this one does not have a simple fix!

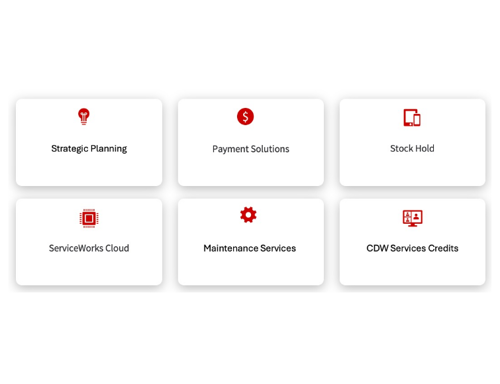

As with many challenges of this scale, working for CDW and having access to our global reach and relationships does allow us to provide a unique set of capabilities to help mitigate the impact. The six elements summarised below can be leveraged as needed to help build your mitigation plan.

Contributors

-

Rob Sims

Rob SimsChief Technologist - Hybrid Platforms